Repairing your credit after divorce

August 14, 2024

Financial planning can become a daunting task as you enter retirement. For many, retirement comes with added financial difficulties like living off a fixed income, managing debt and using services put in place specifically for seniors.

This comprehensive guide offers helpful information and advice for navigating your finances as you age and will help you organize, plan and prepare for the future. Read on to learn more, or click the through the menu below to find out what you're interested in.

Organization is key to managing finances, particularly in retirement. After retirement, you will likely live off a relatively fixed income. This means you’ll need to have a stable budget in place and all financial decisions organized in order to maintain your current lifestyle.

To help keep track of your important financial information, consider keeping a notebook or folder. Writing down important financial information can help you record your finances during retirement and help your family locate it in an emergency.

If you decide to create a notebook with your important financial information, consider letting a trusted relative or friend know where you plan to keep it. If you forget a piece of information or in case of emergency, having a trusted person be able to locate your notebook will be helpful.

Other ways to organize your financial information include:

The Boston College Center for Retirement Research has studied the effects of cognitive aging on an individual’s capacity to personally manage their finances. In a 2017 brief, they concluded that:

To prepare for the possibility of cognitive decline, it’s important to take certain steps to protect yourself, your family and your finances. Always communicate with your family about your finances, consider using a professional financial consulting service and discuss the possible need for a Power of Attorney.

There are many resources and services available for seniors in need of expert financial assistance. One of the most important decisions to be made in regards to financial management for seniors concerns a Power of Attorney (POA) document. This document allows an individual, usually elderly, to select another trusted person to act for them when managing their finances.

A Power of Attorney is helpful in allowing a senior’s individually owned assets and finances to be maintained by someone with better ability to make financial decisions. POA documents can be written to become effective immediately, meaning they are not unreasonably difficult to obtain and can help get a senior help quickly.

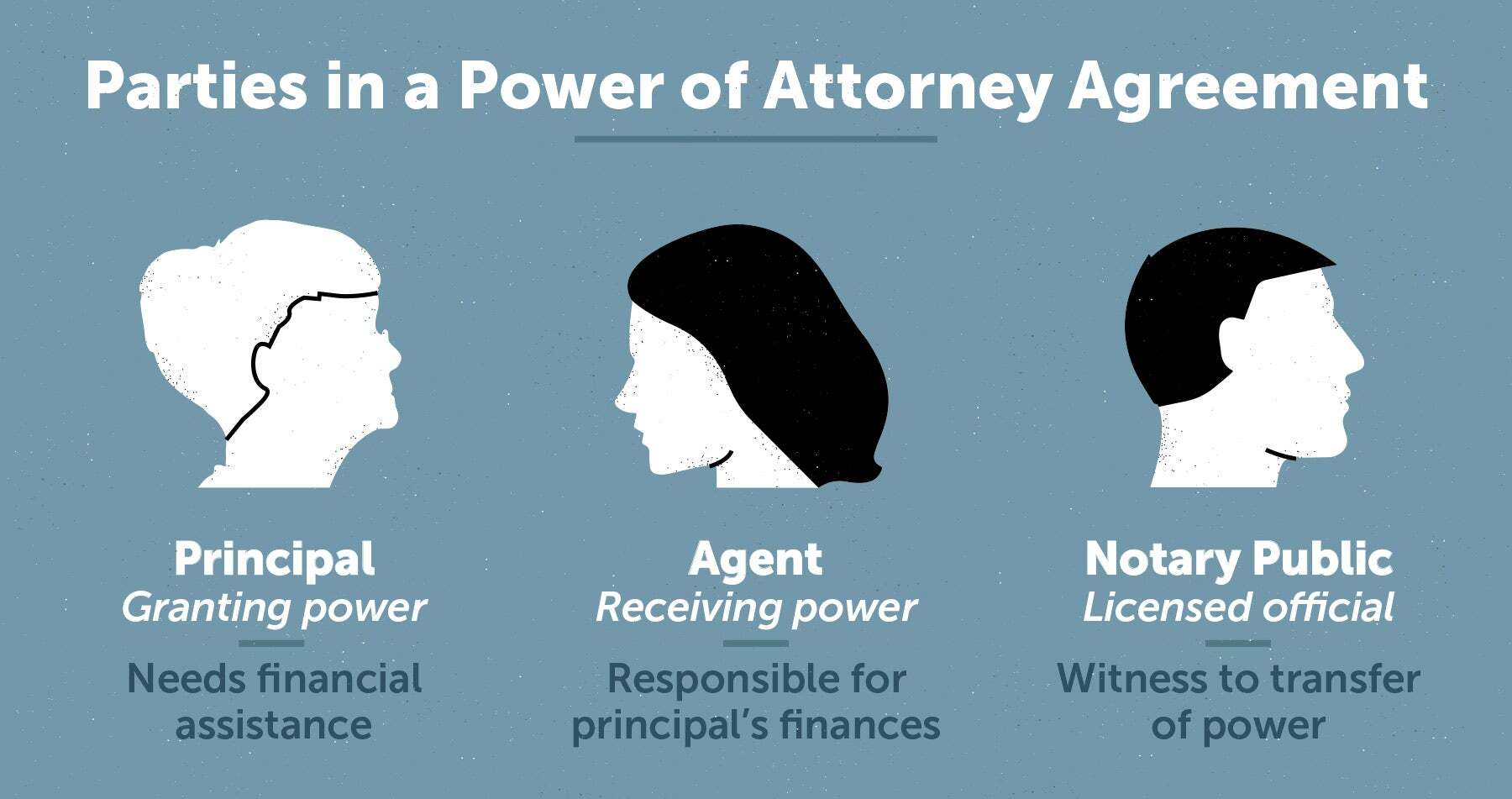

When creating a POA document, there are three main parties involved:

The principal party is the individual giving up power. They may also be referred to as the grantor or donor. In this context, the principal is the senior in need of financial assistance.

The agent, or person receiving power, is the individual who will assume responsibility for the principal’s finances. Any adult can be appointed and in the context of aging, typically falls to the adult child or other relative of the senior giving power.

Finally, the notary public is the licensed official who serves as a witness to the transfer of power. They are typically authorized by a state government and are a required party to the creation of a POA document.

It is important to note that while legal counsel in the creation of a POA document is not necessary, it may be helpful in ensuring the best decisions are made surrounding the transfer of power.

Creating a Power of Attorney document is a proactive way to manage your finances as you age. However, be careful to build the contract appropriately and willingly.

Here are some tips to help you understand, create and use a POA for your finances:

There are many services available to help you organize and plan your retirement life. However, there are steps you should take to be sure your finances fit into your future goals for retirement like travel, investment and helping family.

In your retirement years, you rely on a lower income than you did in your earning years. To make your nest egg last, it can be helpful to create a detailed budget and stick to it.

To begin preparing a retirement budget, you should collect recent bank statements, credit card statements, pay stubs and tax returns. These will be helpful in determining how your expenses will be covered.

Next, list any expenses you plan for on a monthly basis as well as a small fund for emergency use.

Expenses to include in your retirement budget may include:

Calculating your monthly budget can be done by simply subtracting your total monthly expenses from your monthly income. If you’re unsure how to create a budget or would prefer to have a professional help you, there are many ways to make sure your budget accurately reflects your retirement lifestyle.

There are also many resources available to use as templates for budget creation.

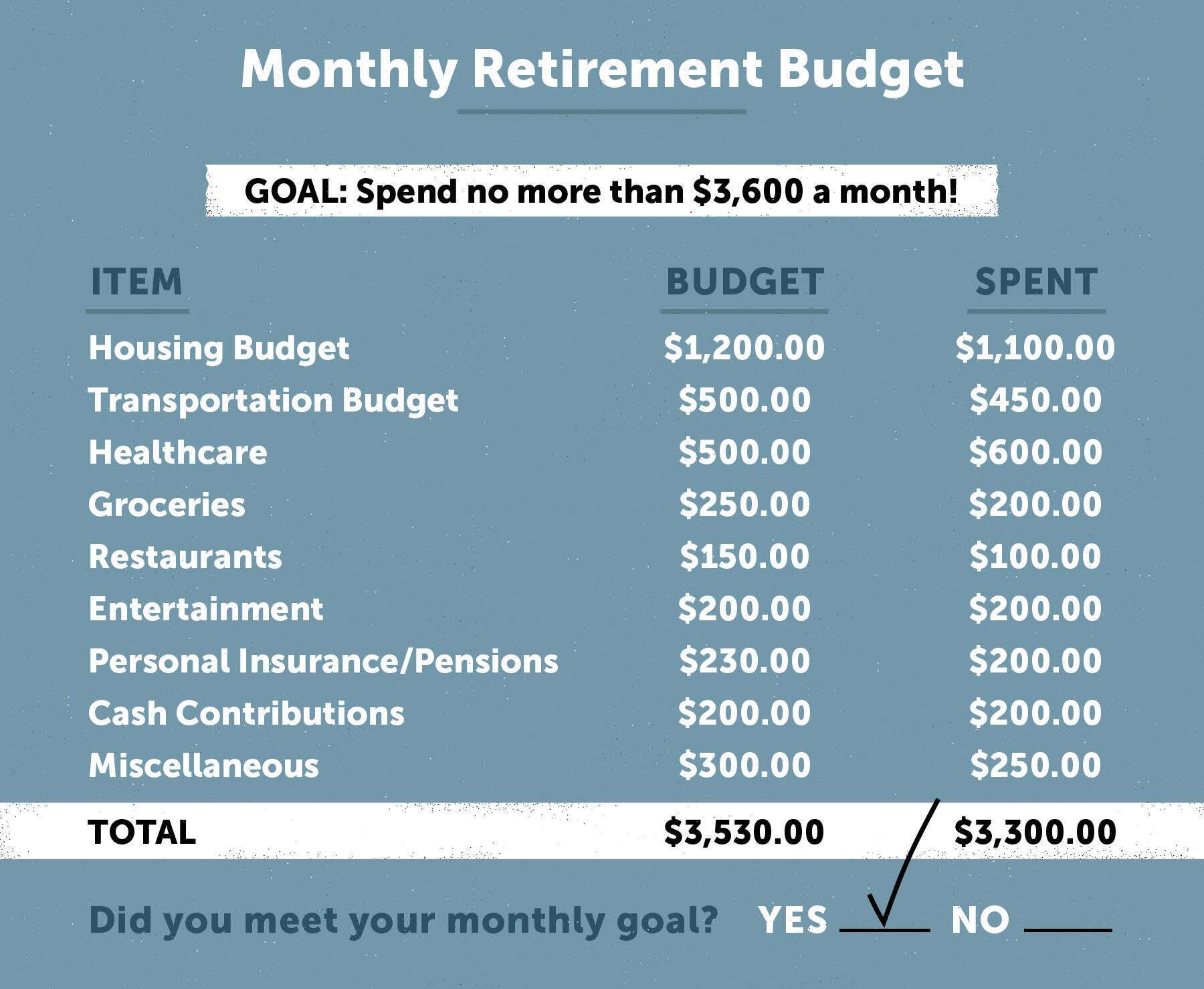

Here is an example of a simple monthly budget for a retiree aged 65 who plans to live in retirement for twenty years. With a monthly budget goal of spending no more than $3,600, he should expect to spend no more than $43,200 annually and no more than $864,000 over the course of his twenty year retirement.

Retirement is not always as simple as you might think. Often, new retirees are shocked to find out that the cost of retirement may be more expensive than planned for.

To budget exactly how much you’ll need for a comfortable retirement, you’ll need to understand your likely retirement expenses. It’s safe to estimate on the high end for all expenses. Along with what you think you’ll spend, you should plan to have additional money set aside in case your expectations are wrong. Don’t plan to spend much less than you do now.

There are a few questions you should ask yourself before you begin budgeting for retirement.

Determine what your monthly expenses will be by considering things like health care and insurance, travel, housing, auto loans and any other miscellaneous costs.

Developing a spending plan can also help curb unnecessary costs and keep your spending habits in check while helping you save for unexpected situations. There are many easy ways you can cut down on your expenses without putting a dent into your comfort.

Consider some of the following methods for decreasing your monthly spending:

Additionally, you should consider the cost of living in your state. The average cost to retire comfortably varies greatly across the states, so it may be helpful to consider moving if you’re worried about funds.

Here are the yearly costs to live comfortably in each state, ranked from least expensive to most.

| Rank | State | Yearly cost | Rank | State | Yearly cost | |

| 1 | Mississippi | $37,750.00 | 27 | South Dakota | $49,344.00 | |

| 2 | Arkansas | $38,896.00 | 28 | Oregon | $49,678.00 | |

| 3 | Alabama | $39,170.00 | 29 | Wyoming | $50,409.00 | |

| 4 | Oklahoma | $41,223.00 | 30 | Pennsylvania | $51,108.00 | |

| 5 | South Carolina | $41,583.00 | 31 | Montana | $51,505.00 | |

| 6 | Kentucky | $41,610.00 | 32 | Virginia | $52,040.00 | |

| 7 | Idaho | $42,066.00 | 33 | Illinois | $52,215.00 | |

| 8 | North Carolina | $42,224.00 | 34 | California | $52,284.00 | |

| 9 | Louisiana | $42,726.00 | 35 | Rhode Island | $53,068.00 | |

| 10 | Tennessee | $42,774.00 | 36 | Colorado | $53,310.00 | |

| 11 | West Virginia | $42,023.00 | 37 | Delaware | $53,585.00 | |

| 12 | Arizona | $43,225.00 | 38 | Washington | $53,653.00 | |

| 13 | Georgia | $43,321.00 | 39 | Maine | $53,776.00 | |

| 14 | Utah | $43,893.00 | 40 | Minnesota | $54,913.00 | |

| 15 | Indiana | $44,541.00 | 41 | Maryland | $55,935.00 | |

| 16 | New Mexico | $44,624.00 | 42 | Hawaii | $56,404.00 | |

| 17 | Kansas | $44,980.00 | 43 | New York | $58,633.00 | |

| 18 | Nevada | $45,221.00 | 44 | Vermont | $59,560.00 | |

| 19 | Texas | $45,671.00 | 45 | North Dakota | $60,281.00 | |

| 20 | Iowa | $46,256.00 | 46 | Connecticut | $60,621.00 | |

| 21 | Ohio | $46,811.00 | 47 | New Hampshire | $61,013.00 | |

| 22 | Missouri | $46,908.00 | 48 | New Jersey | $61,215.00 | |

| 23 | Florida | $48,305.00 | 49 | Alaska | $61,934.00 | |

| 24 | Wisconsin | $48,485.00 | 50 | Massachusetts | $64,976.00 | |

| 25 | Nebraska | $48,713.00 | 51 | Washington DC | $71,054.00 | |

| 26 | Michigan | $49,165.00 |

Many seniors find themselves in retirement with difficulty maintaining their lifestyle. If you are struggling to find a way to continue saving money, some of these options may be helpful: